Open Banking has been talked about for many years, for both personal and business finance, but has it made any real difference? Adam Massias, Data Scientist at Recognise Bank, explains how it could be finally ushering in a quiet revolution for SMEs.

Open Banking began life in 2016 when the Competition and Markets Authority (CMA) published a report into the UK retail banking sector which found that the bigger, more established banks did not have to compete hard enough to win customers, while newer banks found it difficult to access the market.

To address the problem, Open Banking was created as a way for personal banking customers and SMEs to share their financial data securely with third party providers, to drive competition in the market and further the evolution of financial technology to enhance customer experience.

The development of Open Banking based services is particularly good news for small and growing businesses, who have been underserved by the big UK banks for many years. The lack of personal support for SMEs from the providers that dominate the UK business banking sector has meant it has become increasingly hard for smaller firms to find suitable products and services. This is particularly true for SMEs seeking lending, which in turn can limit their growth potential and the opportunity to pursue profitable ventures.

While there are a number of smaller and non-bank lenders serving the SME sector, loan applications and ongoing management can be a time-consuming and fragmented process, involving a lot of different steps for both the customer and the lender. These pain points have been exacerbated by some lenders often using manual and tedious processes that are old-fashioned, convoluted, and most of all, time consuming.

Open Banking can provide solutions and systems that will help alleviate these lending pain points for both customers and lenders.

What is Open Banking?

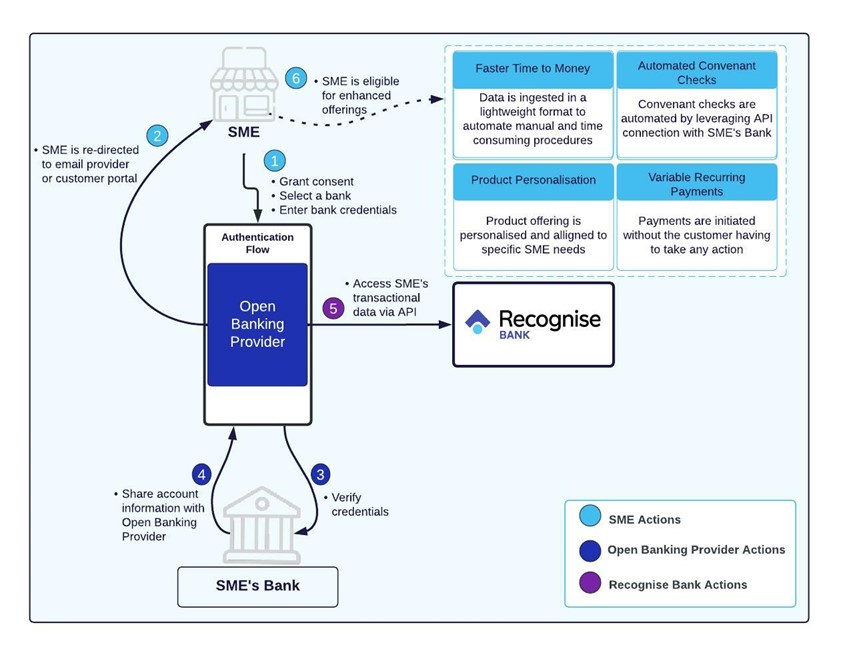

In the past, a customer’s financial data has primarily been taken by large financial organisations, such as a company’s main business bank, with the full picture of an SME’s finances being siloed across a number of platforms, making it difficult to consolidate and analyse. Now, with Open Banking, SME’s have the power to decide which third party providers they share their financial data with and how it is used to benefit the business.

In simple terms Open Banking is a way of SMEs securely sharing their banking data with third party providers – often competitors to their main business bank – with that information being used to drive intelligent personalisation, process automation, and enhanced product offerings. In short, Open Banking is a driving force for innovation for SME banking.

More granularly, Open Banking is the use of open application programming interfaces (APIs) that allow a properly licensed company to securely access customer data, with that company then using that data to provide financial applications and services.

There are two types of Open Banking licenses:

- Account Information Service Provider (AISP) – Whereby a third party is authorised to retrieve account level data from a bank or financial institution

- Payment Initiation Service Provider (PISP) – Which authorises a third party to initiate payments on behalf of a customer

You can think of APIs as a way in which two systems exchange data with one another, in a secure method. Open Banking APIs have been developed by the banks themselves following best practice security standards to ensure a secure and reliable exchange of data, so rest assured your data is safe and remains your property.

The process in which an SME gives consent for its data to be accessed has two steps;

- Authentication – Your bank will request authentication from you to confirm that you are the owner of the account via a login page

- Consent – A brief explanation of the data to be shared and processes that it will be used for

The full journey for AISP (Account Information Service Provider) consent usually takes around thirty seconds and, best of all, requires no paperwork.

How does Open Banking help?

More than just being a description for an ecosystem of apps and services, Open Banking has become synonymous with a philosophy of making the banking sector truly open by allowing new providers to develop new and better solutions.

The depth and quality of data that can be accessed via Open Banking is identical to the legacy process of producing PDF reports or reams of spreadsheets. The beauty of retrieving data via APIs is that it can be automatically sourced in near real-time and in a specific format such as JSON (JavaScript Object Notation), that is easily readable by systems capable of analysing and making intelligent recommendations. Time and manual effort is cut significantly for both parties involved in a financial transaction, the customer and the provider.

Faster Lending

For example, for a lender like us, rather than Business Development Managers and underwriters having to manually review a list of hundreds or thousands of transactions line by line, a model developed based on Open Banking data can discover trends or highlight anomaly transactions to assist with efficient decision making.

The ability to retrieve and process data eliminates tedious manual workloads for both customers and lenders, which means a faster application process and quicker time for the SMEs to receive their funds. It could also mean better rates for customers, automated ongoing checks throughout the life of the loan to ensure it is performing well, and most importantly, a greatly enhanced customer experience.

Personalisation on product offering

Personalisation has come a long way from simply putting someone’s name on an email, and over the past decade some industries, such as marketing, have realised the benefits of personalisation to customers. By contrast, banking has been seriously behind the curve in using its data resources to create personalised customer experiences and products.

However, now key performance indicators and analytical models can be used to review raw Open Banking data can help to build insight of a business’s affordability, concentration risk, expense and income patterns, in a depth that has not previously been seen. Leveraging this depth of insight, providers can now offer products and lending terms that are personalisedto each individual SME’s financial situation and growth needs in a way that hasn’t been done before.

Automated payments with VRPs

The most common method of payment collection for SMEs is Direct Debit (DD) or Continuous Payment Authority (CPA), but while these methods have been widely used for many years, they both have well known defects.

Variable Recurring Payments (VRPs) are here to save the day! These are consent based variable amount payment instructions, again made possible through Open Banking. SMEs can safely connect PISPs (Payment Initiation Service Provider) to their bank account so that they can make payments on their behalf.

Why are VRPs gaining so much traction?

- They use the faster payment scheme

- They are protected under the payments services regulation, so safer for customers

- They can be of variable amounts, within a pre-defined boundary

Unlike other payment methods, VRPs allow SMEs to have a crystal-clear view of when, how much, and why payments are being taken, and at the same time eliminate any manual intervention when rates or schedules change.

What’s next?

With its strong regulatory foundations, established security features, and ability to enhance many of the processes on both sides of the financial transaction, Open Banking is poised for mainstream adoption by financial institutions and customers.

At Recognise Bank, our understanding of SMEs and the insight we gain from working closely with them, gives us a clear view of their challenges and areas where support is needed. Open Banking provides us with the means to create innovative services and products to meet those challenges.

We think Open Banking is an exciting evolution for SME banking and we are committed to continuing our development and research with Open Banking technologies, bringing new developments to our customers that we believe will be of benefit to them.

Reference: Variable Recurring Payments. What are they and how can they help SMEs? – Open Banking